SBA 7(a) Loans for Liquor Stores

Liquor store financing for business owners

Experience Ready Capital’s commitment to liquor store business owners and investors. We close SBA 7(a) deals that other lenders can’t, working with a range of credit scores and financing challenges.

Whether clients are buying or expanding their liquor store businesses, Ready Capital can help them get the financing they need—even in the current market.

Why Ready Capital

- A value-add lender, closing more deals with credit flexibility

- Trust and confidence in execution

- Centralized front-end reviews, closers involved early

- #4 SBA Preferred Lender in the U.S.

Liquor store financing highlights

- Loans to $5 million

- Terms up to 25 years

- Low borrower equity required

- Flexible use of loan proceeds

- Limited/No prepayment penalties

- Closing costs may be financed

Loan terms vary by loan program, borrower eligibility, loan amount, and other factors.

Liquor store loan purposes

- Business acquisitions

- Real estate purchases

- Store expansions

- New equipment purchases

- Working capital

MARKET FACTS

of the beer, wine, and liquor stores industry in the U.S.

increased faster than the economy overall.

Source: IBISWorld, 2023

Have a question about liquor store SBA 7(a) Loans?

FAQs

What is liquor store financing?

Answer: Liquor store financing is specifically designed for individuals or entities looking to buy and operate a liquor store. It involves loans to cover the costs associated with starting and running a liquor store business.

What types of financing options are available for liquor stores?

Answer: There are several liquor store business lending options, including traditional bank loans, SBA 7(a) loans, equipment financing, and lines of credit. The choice of financing depends on the business owner’s needs and financial situation.

What is an SBA loan, and what are the key benefits for liquor stores?

Answer: An SBA loan is a type of loan backed by the Small Business Administration that helps small businesses, including liquor stores, get the financing they need.

The benefits of SBA loans for liquor stores include:

- Lower down payments (typically 10%)

- Longer repayment terms (up to 25 years)

- Competitive interest rates

- Flexible use of funds

- Access to expert guidance and resources from the SBA

Learn more about how SBA loans work.

What can liquor store financing be used for?

Answer: Liquor store financing can typically be used for business acquisitions, real estate purchases, store expansions, new equipment purchases, and working capital.

Do I need to have prior business experience to qualify for a liquor store loan?

Answer: While prior business experience can be beneficial, it’s not always a strict requirement.

What are the SBA requirements for liquor store loans?

Answer: SBA loan requirements can vary, but in general, lenders consider these factors:

- Personal and business financial statements

- A comprehensive business plan

- Financial projections

- Business track record

- Resumes of key team members

- Personal credit history and scores

- Collateral

What collateral might be required for financing a liquor store?

Answer: Collateral requirements vary from lender to lender. Common types of collateral may include personal assets like real estate, equipment, or business assets. The specific collateral requirements will be outlined in the loan agreement.

How long does it take to get approved for an SBA loan for my liquor store?

Answer: The approval timeline can vary but it typically takes anywhere from a few weeks to a few months. Delays may occur if additional documentation or information is required, so it’s essential to start the application process early.

What should I look for in a liquor store lender?

Answer: When exploring lenders, consider their experience, available financing options, and their track record of successful lending to liquor store businesses.

SBA Preferred Lenders are experienced in aligning borrowers with their business goals and guiding them through the SBA application process.

Get Started

Apply for a Ready Capital SBA 7(a) loan

Click the button to start the application process. It takes less than 3 minutes and will not affect your credit score.

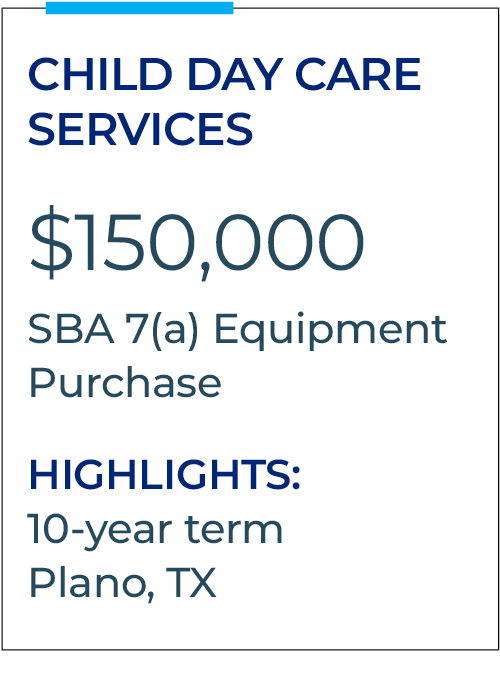

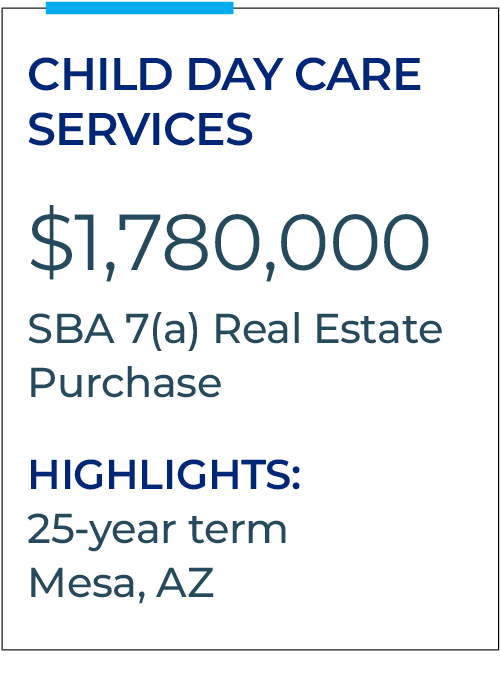

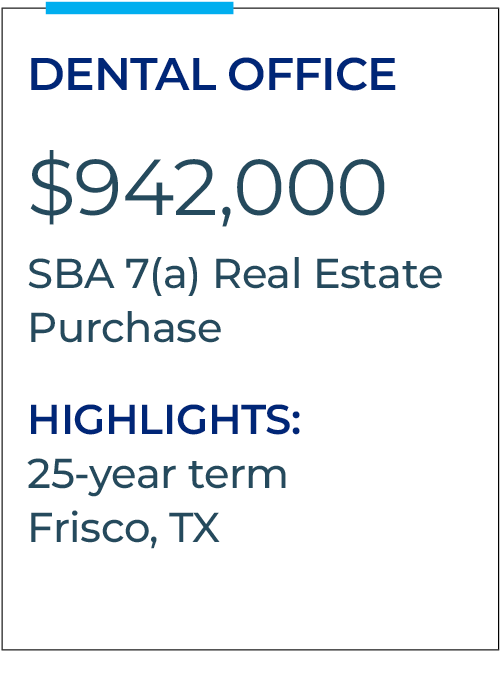

Recent Transactions - All Industries